In 2020, the SEC modernized the disclosure requirements for acquisitions and dispositions under Rule 3-05 and Article 11 of Regulation S-X. The goal was to reduce the burden on registrants while ensuring investors receive material data. For middle-market firms eyeing a liquidity event or public offering, understanding these thresholds is a pillar of transaction readiness.

Following the SEC’s compliance guidance, here is how Diedrich Consulting helps you navigate the “significance” tests and the resulting disclosure obligations.

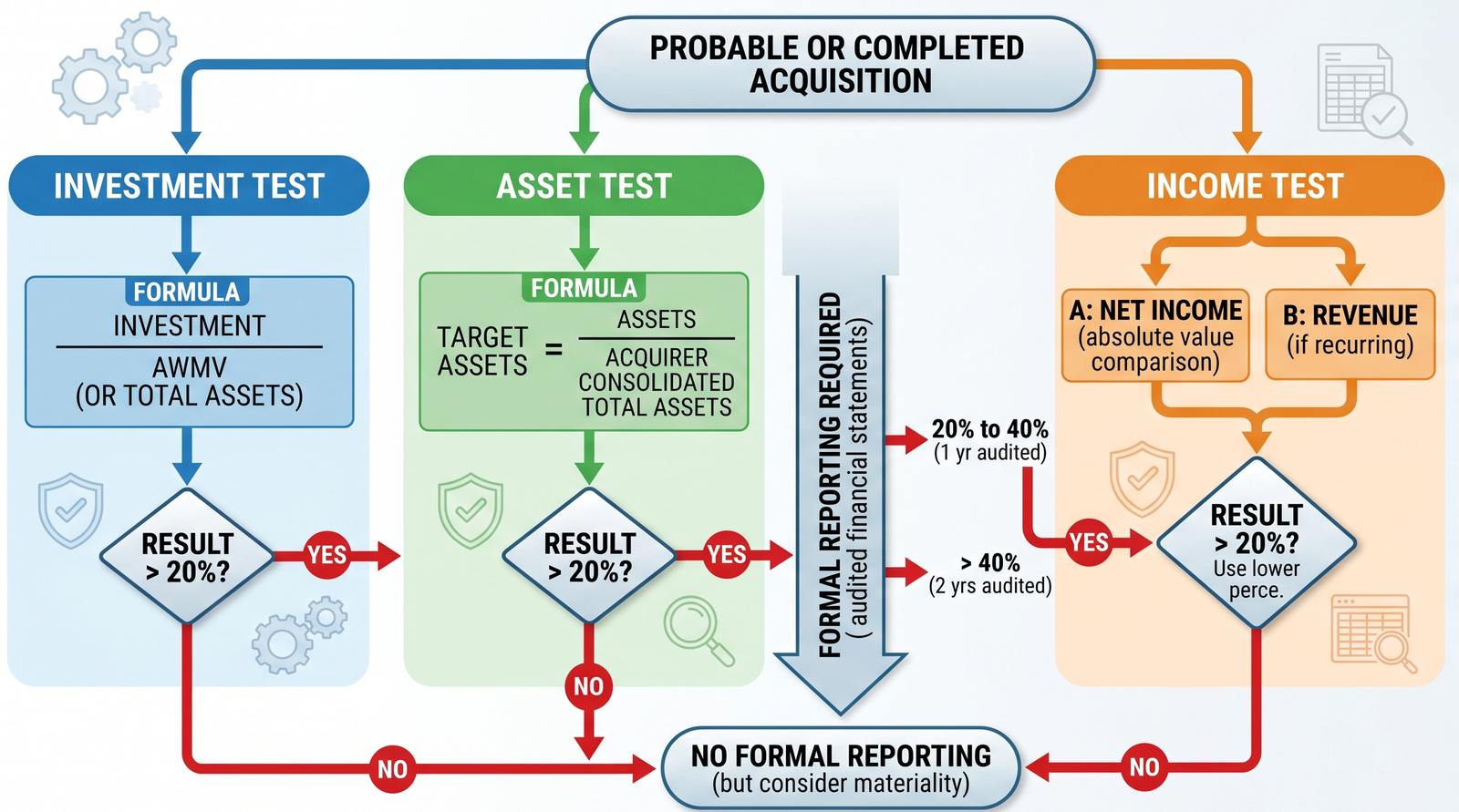

The Three Significance Tests: Are You Over the 20% Limit?

To determine if a target’s financial statements are required, the SEC mandates three specific tests. If the acquisition exceeds 20% on any of these tests, formal reporting requirements are triggered.

1. The Investment Test

This measures the economic scale of the deal.

- The Formula: Compares the purchase price (consideration transferred) to the Aggregate Worldwide Market Value (AWMV) of the acquirer’s common equity.

- Key Detail: If the acquirer has no AWMV, the test defaults to comparing the investment to the acquirer’s total assets.

2. The Asset Test

This measures the physical footprint of the acquisition.

- The Formula: Compares the acquirer’s share of the target’s total assets to the acquirer’s consolidated total assets as of the most recent fiscal year-end.

3. The Income Test (The Two-Pronged Approach)

The income test was recently updated to include a Revenue Component to reduce volatility for companies with fluctuating earnings.

- Prong A (Net Income): Compares the absolute value of the target’s income/loss from continuing operations to the acquirer’s.

- Prong B (Revenue): Only applies if both entities have recurring annual revenue.

- The Result: If both prongs are met, the lower of the two percentages determines significance.

Tiered Disclosure Requirements

Once significance is calculated, the SEC outlines specific requirements for audited historical financial statements:

| Significance Level | Requirement |

|---|---|

| 20% to 40% | 1 year of audited financial statements for the target. |

| Over 40% | 2 years of audited financial statements for the target. |

Export to Sheets

The “Individual vs. Aggregate” Rule: If you close multiple small acquisitions that are individually below 20% but collectively exceed 50% significance in a year, the SEC requires audited financials for the substantial majority of those businesses.

Pro Forma Information: Article 11 Adjustments

Beyond historical data, the SEC requires Article 11 Pro Forma statements to show the “Combined Co” outlook. Modernized rules categorize adjustments into:

- Transaction Accounting Adjustments: Reflecting the application of required accounting (e.g., purchase price allocation).

- Autonomous Entity Adjustments: Necessary if the target will incur new standalone costs (e.g., leaving a parent company).

- Management’s Supplemental Adjustments: An optional way for management to show expected synergies and cost-savings.

Diedrich Consulting: Your Partner in M&A Compliance

The SEC provides the what, but Diedrich Consulting provides the how. Many firms struggle with the Income Testspecifically when dealing with adjusted EBITDA or non-recurring items.

Our M&A Advisory Services include:

- Significance Modeling: Running the three SEC tests during the LOI stage to predict reporting hurdles.

- S-X Compliance Mapping: Ensuring target audits meet SEC standards, which often differ from private company GAAP.

- Article 11 Preparation: Drafting pro forma financials that clearly communicate the deal’s value to investors.

Don’t let reporting delays derail your close. Contact Diedrich Consulting today to ensure your acquisition accounting and SEC disclosures are airtight.